PAT replaces bank account credentials with unique, non-sensitive account tokens which are different for each use case, e.g. consumer-to-business (C2B), peer-to-peer (P2P), request-to-pay (RfP), open banking or specific for payee/payer. The solution can be applied in different payment flows without major impact to the flows or messages.

Financial institutions can trace account tokens and verify consent given to third parties for storing these tokens via a specific token attribute.

PAT lets financial institutions gain control as they can set token-level payment controls, which allows them to suspend specific tokens in case of fraud. By suspending specific tokens rather than the full account, other transactions will not be impacted.

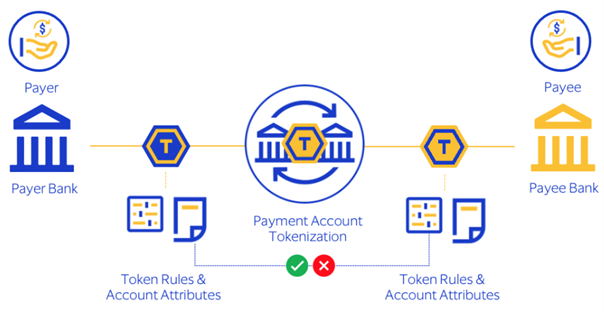

Financial institutions will set rules for how tokens can be used in different payment use cases (e.g. C2B, fintech, wallets) via token rules. Token rules are used to define how the payment is being used, such as setting what type the receiving account is, the type of payment, which payment rails are allowed, what the payment value limits are, what the payment frequency is, and perform a full account name match. Token rules are validated against payment message data, counterparty bank account attributes, and token status. Token validation results are returned to the bank, along with the token attributes at the time of payment, to enable the bank to make informed decisions on whether the token is used for the payment as intended.

PAT provides several benefits to banks and financial institutions:

PAT allows financial institutions to know where account tokens are stored with consent for use in payments or money movement, building client confidence.

Financial institutions can suspend a specific token, helping reduce payment reversals and reimbursement requests by enabling a stop on specific token payments when payment terms, breaches, or fraud risk require it, rather than impacting the full account.

Financial institutions can limit tokens for only push or pull payments, single-use or recurring payments, a specific merchant, region, currency, payment value limit, or frequency, ensuring each token is used only as intended.

Financial institutions have more information about the account they are about to send money to or receive money from, such as merchant category, account type (personal, business, charity), time in good standing, velocity parameters, etc., helping them make more informed payment decisions.

Financial institutions can set acceptable risk and liability levels for each token based on the account insights they gain access to through tokens, making payments more resilient to fraud and reducing false positives.

Start a Project

Start a Project